Int. J. Financial Stud. 2024, 12(1), 5; https://doi.org/10.3390/ijfs12010005 - 12 Jan 2024

Abstract

►

Show Figures

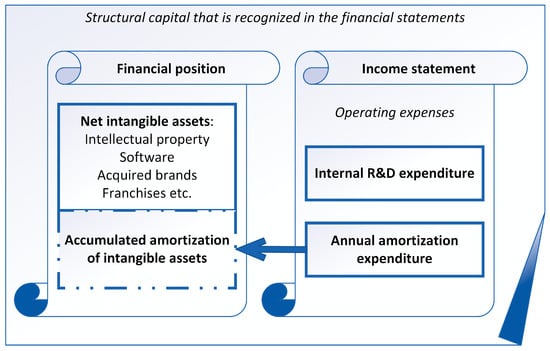

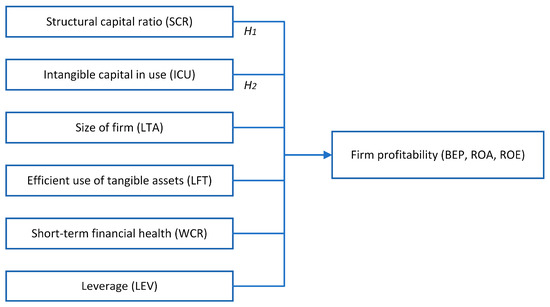

The aim of the present study is to assess the impact of structural capital intensity and utilization on firm profitability in an international setting: the European Union countries, plus Norway, Switzerland and the United Kingdom. The indicators are calculated based on financial data

[...] Read more.

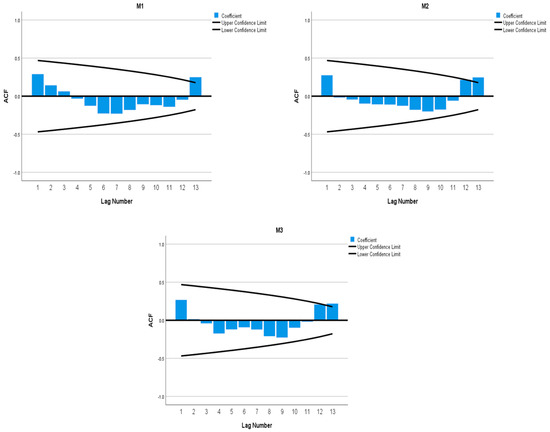

The aim of the present study is to assess the impact of structural capital intensity and utilization on firm profitability in an international setting: the European Union countries, plus Norway, Switzerland and the United Kingdom. The indicators are calculated based on financial data downloaded from the Refinitiv Eikon database. Two financial ratios are used as proxies for the intensity and utilization of structural capital. The balanced panel consists of 625 companies from 25 countries, over the period from 2013 to 2022. The panel includes financial information on two industries that are considered innovation-oriented, namely technology and healthcare. Alternative model specifications are proposed to test the robustness of the basic model, including dynamic models (with lagged dependent variables). The present study indicates that a higher proportion of structural capital (intangible assets, excluding goodwill) is a negative factor for company profitability in the technology and healthcare sectors. There is no indication that a more intense use of intangible assets and more investments in R&D positively contribute to company profitability in the respective industries, for a large sample of listed companies. A higher proportion of intangible assets, as reported in financial statements, is possibly related to inefficiencies in the management of structural capital. The inverse relationship between profitability and investments in intangible assets is likely due to failures in cost accounting. Limitations and future research propositions are provided in the conclusions.

Full article

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}